The 52-week money-saving challenge is one of the most popular savings methods in personal finance and for good reason. It works. It’s simple. It builds the savings habit gradually instead of demanding perfection from week one. And by the time December arrives, most people have saved more than they ever thought they could.

If you’ve tried to save money before and quit, this challenge is designed for people exactly like you. The structure does what willpower can’t it gives you a specific number to hit each week so you never have to wonder how much to set aside.

This guide gives you the complete 52-week challenge breakdown, three versions to choose from based on your income, a penny saving challenge option for absolute beginners, tips to stay on track, and the free printable you can use to track every single week.

How to Download the Free 52-Week Savings Printable

Step 1:

Scroll down to the button in this article and click “Click Here to Download Free Printable”

Step 2:

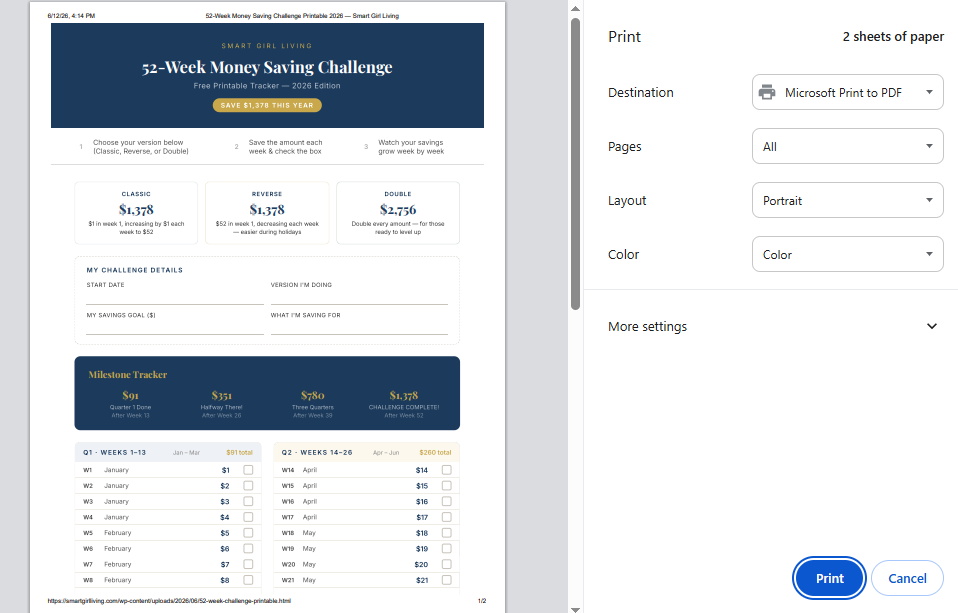

A new page will open showing the printable tracker. Click the “Download / Print Tracker”

Step 3:

Your browser’s print window will open. Make sure Destination is set to “Microsoft Print to PDF” and Color is set to “Color”. Then click Print.

Step 4:

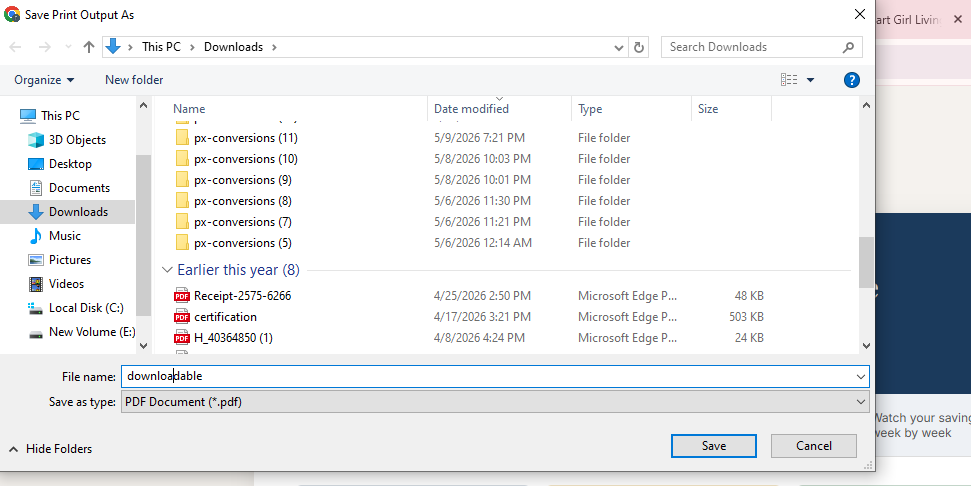

A save dialog will open. Choose your folder, name the file (example: “52-week-challenge-printable”), and click Save. Your PDF is now saved to your computer, ready to print!

What Is the 52-Week Money Saving Challenge?

The 52-week money saving challenge is a weekly savings plan where the amount you save increases by $1 each week throughout the year. Week 1 you save $1. Week 2 you save $2. Week 52 you save $52.

By the end of the year, you’ve saved $1,378.

It’s not a life-changing amount on its own but that’s not the point. The point is that you’ve built a real, consistent money saving habit that you can scale up. The person who completes the 52-week challenge in year one typically doubles or triples their savings target in year two. The habit compounds even when the dollar amounts start small.

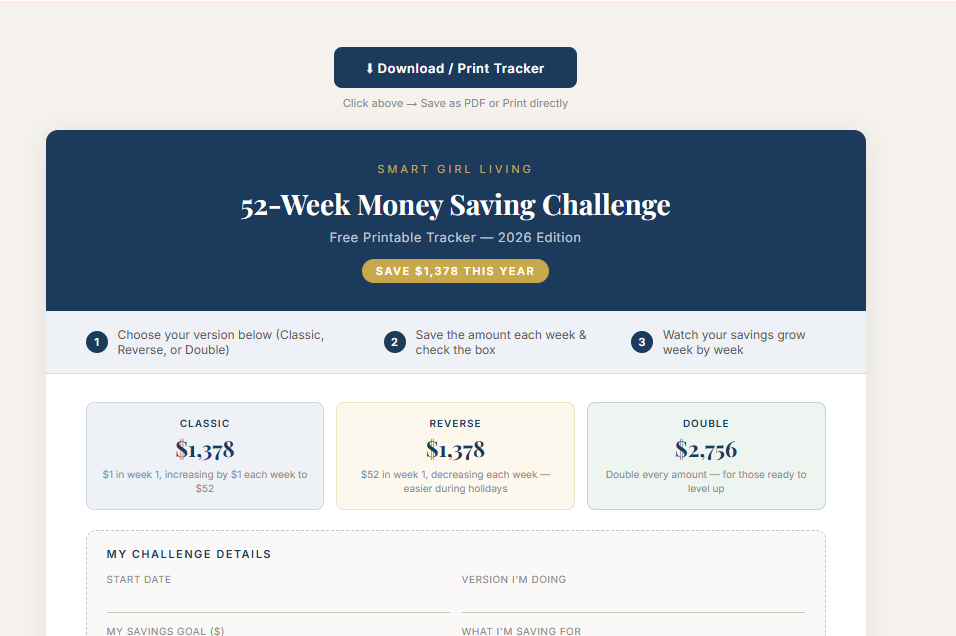

The Classic 52-Week Challenge: Full Breakdown

Here is every week of the classic challenge:

Weeks 1–13 (January–March): Week 1: $1 | Week 2: $2 | Week 3: $3 | Week 4: $4 | Week 5: $5 | Week 6: $6 | Week 7: $7 | Week 8: $8 | Week 9: $9 | Week 10: $10 | Week 11: $11 | Week 12: $12 | Week 13: $13 Running total: $91

Weeks 14–26 (April–June): Week 14: $14 | Week 15: $15 | Week 16: $16 | Week 17: $17 | Week 18: $18 | Week 19: $19 | Week 20: $20 | Week 21: $21 | Week 22: $22 | Week 23: $23 | Week 24: $24 | Week 25: $25 | Week 26: $26 Running total: $351

Weeks 27–39 (July–September): Week 27: $27 | Week 28: $28 | Week 29: $29 | Week 30: $30 | Week 31: $31 | Week 32: $32 | Week 33: $33 | Week 34: $34 | Week 35: $35 | Week 36: $36 | Week 37: $37 | Week 38: $38 | Week 39: $39 Running total: $780

Weeks 40–52 (October–December): Week 40: $40 | Week 41: $41 | Week 42: $42 | Week 43: $43 | Week 44: $44 | Week 45: $45 | Week 46: $46 | Week 47: $47 | Week 48: $48 | Week 49: $49 | Week 50: $50 | Week 51: $51 | Week 52: $52 Running total: $1,378

The challenge with the classic version is that weeks 40–52 fall during the holiday season, exactly when most people’s budgets are tightest. That’s why there are two more versions worth knowing about.

Version 2: The Reverse 52-Week Challenge

The reverse version starts with your biggest deposits in January and decreases each week throughout the year. Week 1 you save $52, week 2 you save $51, and so on down to $1 in week 52.

Why it works better for some people: January is typically when motivation is highest and holiday spending has stopped. You front-load the hardest weeks when energy is strongest, and coast through December with $1–$5 weekly deposits when your budget is under the most pressure.

The total saved is identical: $1,378.

If you tend to start strong and struggle in the second half of the year, the reverse version is almost certainly the better fit.

Version 3: The Modified Challenge (Double the Savings)

For anyone whose budget can handle more, the modified challenge simply doubles every amount. Week 1 is $2, week 2 is $4, week 52 is $104.

Total saved by December: $2,756.

This version works well for people who’ve completed the classic challenge before and want to scale up, or for households where two people are doing the challenge together and pooling their weekly contributions.

The Penny Saving Challenge: For Absolute Beginners

If $1 a week still feels like too much to commit to right now, the penny saving challenge is where to start.

Day 1 you save 1 cent. Day 2 you save 2 cents. Day 365 you save $3.65.

By the end of the year, you’ve saved $667.95 from pennies. It sounds almost too small to matter, but the penny saving challenge is genuinely useful for two reasons: it builds the daily savings habit in a way that’s completely painless, and it proves to people who’ve never saved consistently that they can do it.

Once you complete a penny challenge year, the 52-week money saving challenge feels completely achievable by comparison.

Free 52-Week Savings Challenge Printable 2026

To track your progress, print this simple tracker. For each week, check the box when you’ve made your deposit.

How to use it: Write your savings amount next to each week number. Check the box when you deposit that week’s amount. Write your running total at the end of each month. Keep it somewhere visible on the fridge, in your wallet, taped to your bathroom mirror.

The printable works for all three versions of the challenge. Just write in your weekly amounts based on which version you’re doing.

The best place to save money for this challenge is a dedicated savings account that’s separate from your everyday checking account. When the money is in a different account, you’re far less likely to dip into it. If you want your savings to earn something while they sit, look for an automatic savings app or high-yield account that doesn’t charge fees your challenge savings deserve to work for you, not just sit idle.

How Much Does the 52-Week Challenge Save?

Classic version: $1,378 Reverse version: $1,378 Modified (doubled) version: $2,756 Penny saving challenge: $667.95

Choose the version that fits your current financial situation honestly. The challenge that you complete is infinitely more valuable than the one you quit in March because it was too ambitious.

The Best Money Saving Apps to Automate Your Challenge

One of the smartest ways to run the 52-week challenge without relying on willpower is to use money saving apps that automate your weekly deposit.

The best money saving apps for this challenge work by scheduling automatic transfers on a set day each week. You set it once, and every week the right amount moves from checking to savings without you thinking about it.

Some automatic savings apps go further they analyze your spending patterns and move small amounts to savings automatically when they detect you can afford it. Apps like Qapital, Digit, and Chime’s automatic savings feature are popular options. They work best when paired with a dedicated savings account for your challenge funds.

The combination of a weekly savings challenge and automation is what separates people who finish the year with $1,378 and people who forget about the challenge by February.

7 Tips to Actually Complete the 52-Week Challenge

1. Automate Every Weekly Deposit

Set up your weekly transfer immediately after reading this. Pick a consistent day; payday works well and automate the deposit so it happens without you remembering. Money-saving becomes significantly easier when it’s automatic.

2. Keep Challenge Money in a Separate Account

Don’t keep your 52-week challenge savings in your regular checking account. Open a dedicated savings account just for this goal. The separation creates a psychological barrier that makes it harder to spend and easier to watch grow.

3. Make It Visual

Print the tracker. Cross off each week as you go. There’s something genuinely satisfying about seeing 30 weeks crossed off that keeps you going through the harder months. Visibility is one of the best ways to stay motivated during any money saving challenge.

4. Do It With Someone Else

Find a friend, partner, or family member who’ll do the challenge with you. Share your progress weekly. The social accountability makes a real difference it’s much harder to skip a week when someone else is watching.

5. Celebrate Monthly Milestones

At the end of each month, acknowledge what you’ve saved. Not with a spending splurge with a moment of genuine recognition that you’re doing something most people don’t. By the end of March, you’ll have $91 saved from almost nothing. That’s worth noticing.

6. Skip Weeks When You Need To (Then Catch Up)

Life happens. A tight week, an unexpected expense, a month that just doesn’t cooperate. If you miss a week, don’t quit just double up the following week. The challenge is flexible. The only way to fail it is to stop entirely.

7. Remember What the Money Is For

The $1,378 at the end of the year should have a job waiting for it. Emergency fund top-up. Holiday spending fund for next year. First payment on a savings goal. Name it before you start the challenge and remind yourself of it whenever motivation dips.

What to Do With Your $1,378 When the Challenge Is Done

The most important thing you can do with your challenge savings is not spend them on something impulse-driven the moment December ends. Have the plan in place before you start.

The most common uses: building or topping up an emergency fund, paying off a small debt, contributing to a holiday spending fund so next December doesn’t feel financially stressful, or rolling it into a bigger savings goal.

If you want to build on this momentum toward a bigger savings target, my guide on how to save $10,000 in a year gives you the month-by-month breakdown for the next level and it pairs perfectly with what you just built.

Combining the 52-Week Challenge With a Budget

The 52-week challenge works best when it’s built into your monthly budget rather than treated as something separate. If your budget doesn’t currently include a weekly savings line, add one now.

If you don’t have a budget yet, building one is the single most impactful thing you can do for your finances not just for this challenge but for every money goal you have. My step-by-step guide on how to make a budget for beginners walks through exactly how to set one up, including how to make room for a savings challenge in your existing expenses.

Common Questions About the 52-Week Money Saving Challenge

Can I start the challenge mid-year? Yes. Start with week 1 regardless of what month it is and work through 52 consecutive weeks from your start date. You don’t have to begin in January.

What if I want to save more than $1,378? Use the modified version (doubled amounts) or run the challenge twice once for a savings goal and once for an emergency fund. Two parallel challenges add up to $2,756 by year end.

Should I use cash or a savings account? A savings account is safer and easier to track. If you’re doing the challenge with cash, use a labeled envelope or jar so the money stays separate and accounted for.

Is the reverse challenge really better? For most people yes. Saving the hardest amounts in January when motivation is highest and budgets are less strained by holiday spending makes completion significantly more likely.

Final Thoughts on the 52-Week Money Saving Challenge

The 52-week money saving challenge isn’t about the $1,378. It’s about proving to yourself that you can save consistently week after week, even when money is tight, even when motivation fades.

Once you have that proof, every savings goal gets easier. The habit is the real prize. The money is the bonus.

Print the tracker. Pick your version. Set up the automation. And check back in 52 weeks to tell me how it went.

For more ways to build savings momentum alongside this challenge, my guide on how to save money fast on a tight budget has 20 strategies you can layer in right now many of which will make hitting your weekly challenge amounts feel much easier.

And if you’re working on paying off debt at the same time as running this challenge, it’s worth reading how to pay off debt fast to understand how to prioritize between the two goals without feeling like you’re spinning your wheels on both.